Sometimes you can quickly lose sight of what is important. Given the horrendous national debt of € 1,973,913,626,707 (01.09.2011 at 09:00 clock), it comes to the healthy budget! In the medium to long-term perspective, the structural budget deficit is crucial.

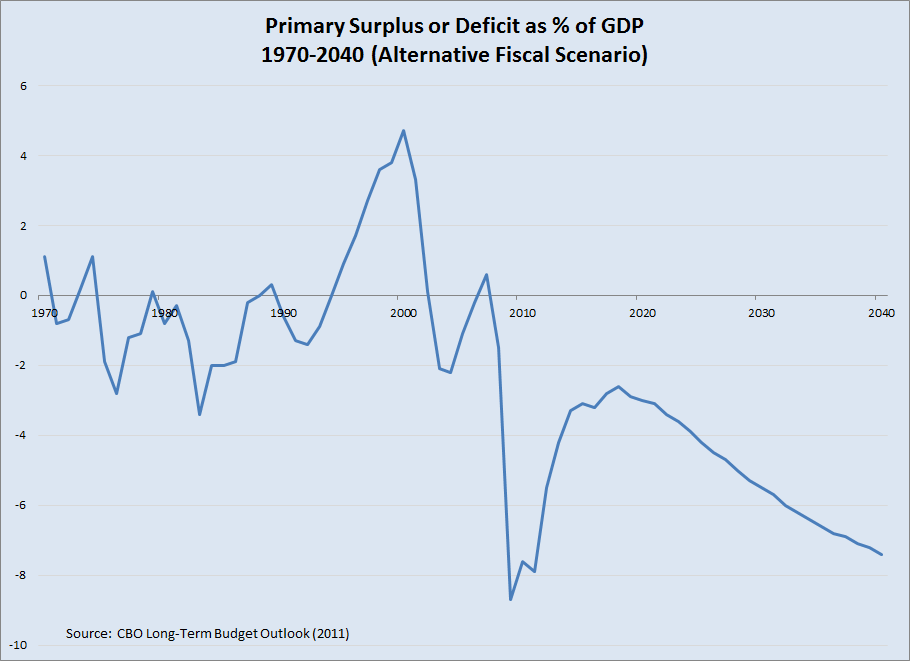

For a sustainable consolidation of public budgets can be meaningfully refer only to a reduction in the structural deficit financing, i.e., adjusted for cyclical effects and one-off measures primary deficit. After structural terms in 2007 and 2008, a balanced general government budget has been reached.  The primary deficit rose to 0.5% significantly in 2009 and -1.3% in 2010. This increase is due to the reduction in the contribution rate for unemployment insurance, which caused in-force of the corporate tax reform, the unsustainable revenue losses because of stimulus programs and the so-called “pension guarantee”.

The primary deficit rose to 0.5% significantly in 2009 and -1.3% in 2010. This increase is due to the reduction in the contribution rate for unemployment insurance, which caused in-force of the corporate tax reform, the unsustainable revenue losses because of stimulus programs and the so-called “pension guarantee”.

With the planned tax cuts of the coalition parties, it is therefore important that these be financed structural and not based on adverse economic pump. It is for an ideally by restraint of the state, by reducing expenditure. A first important and courageous step, for example, would be the repeal of regulatory policy and economically questionable subsidies.

The so-called “Koch-Steinbrück list” here provides some useful  suggestions for spending cuts and numerous examples that have led to windfall gains. The reduction in the structural general government deficit is aimed at achieving long-term goals. In particular the need to avoid excessive burden on future generations. Precisely on this, policymakers should look for in the discussion of the counter-financing of tax cuts.

suggestions for spending cuts and numerous examples that have led to windfall gains. The reduction in the structural general government deficit is aimed at achieving long-term goals. In particular the need to avoid excessive burden on future generations. Precisely on this, policymakers should look for in the discussion of the counter-financing of tax cuts.

This debate is necessary not least in view of the constitutional right of the debt ceiling. The federal government provides for an upper limit of the structural debt of 0.35% of GDP from 2016 and for the countries from the year 2020. The State shall regulate the functioning of social life. The rest of it should be left to the people, but they need of purchasing power.

It is not about any counter-financing, which in turn provide is a risk, when the funding source is low or absent in the future. Economic problems need to be solved completely.